For most general partners, the hard truth becomes obvious fast: raising capital is significantly harder than deploying it. You can be an exceptional investor with incredible access to deal flow, but if you cannot convince Limited Partners to back your vision, your fund will never get off the ground.

When you step into the world of emerging manager fundraising, the rules of the game become immediately clear. LP expectations have shifted. The market is more competitive than ever. LPs are managing their own liquidity, and convincing them to write a check requires more than a good pitch deck. It requires a flawless process.

This guide is for founders and GPs who are actively raising Fund I, II, or III. If you want to replace manual guesswork with a structured, systematic approach, you are in the right place.

We will cover exactly how to define your fund strategy, understand LP evaluation criteria, target the right investors, run an efficient pipeline, and close capital.

We’ll also introduce you to LP Navigator—OpenVC’s new platform for helping emerging managers land limited partners.

Table of Contents

The Reality of Being an Emerging Manager Today

Before you build your target list, you need to understand where you sit in the market. There is a distinct difference between being a first-time fund manager and being an emerging manager with an existing track record.

A first-time manager is often raising on a thesis, angel investments, and a strong professional network.

An emerging manager on Fund II or III has early markup data, distributions, and portfolio companies to point to.

Regardless of which camp you fall into, the current fundraising climate is unforgiving. You are competing against thousands of other funds for a finite pool of LP capital. If you approach a family office with a generic "early-stage B2B SaaS" thesis, you will be ignored. LPs see dozens of those every week.

Building an LP base is a time-consuming grind. Do not sugarcoat this reality for yourself or your team. You will face months of rejections, ghosting, and delayed timelines.

Success belongs to the managers who treat LP fundraising as a disciplined sales pipeline rather than a networking exercise.

Define Your Fund Strategy Before You Raise

Most managers skip the strategic foundation and go straight to outreach. This is a massive mistake. If your fund strategy is loose, LPs will spot it in the first five minutes of a call.

Your fund size dictates your realistic LP base. If you are raising a $10M Fund I, you are not targeting large pension funds or endowments. You are targeting high-net-worth individuals (HNWIs), family offices, and successful tech founders. You need to connect the dots between your check size, portfolio construction, and your required return profile. If you write $250k checks, how many companies do you need to back? What failure rate are you modeling? How big do the winners need to be to return the fund?

Positioning matters. A sharp, niche thesis almost always beats a broad, generalist approach for early funds. LPs use emerging managers for alpha and specific market access. If you focus exclusively on "AI infrastructure for legacy manufacturing," an LP looking for industrial exposure knows exactly why they should allocate to you.

If you need to nail your fundamentals first, take a step back and read our guide on How to Model a Venture Fund. Get the math right before you ask anyone for money.

How LPs Actually Evaluate Emerging Fund Managers

There is a common misconception about how LPs look at emerging fund managers. Many GPs believe that "track record" solely means an institutional investing track record. While having prior top-tier VC experience helps, LPs look for other concrete proof points to mitigate their risk.

The signals that actually matter to LPs revolve around your competitive advantage. They want to see unique access to deal flow. Can you get into competitive rounds that other funds cannot? They want to see a strong founder network. Do top-tier founders actually want you on their cap table? Finally, they demand absolute thesis clarity. You need to know exactly what you invest in and, more importantly, what you pass on.

Getting the first meeting does not require a 40-page deck. You need a tight narrative and a clear right-to-win. Your initial outreach should convey your thesis, your edge, and your target fund size in a few simple sentences. LPs are evaluating your clarity of thought just as much as your investment strategy.

Building Your LP Targeting Strategy

Sourcing capital requires matching your fund strategy to specific LP archetypes. The pitch you give to a family office is fundamentally different from the pitch you give to a fund of funds. Family offices might care deeply about co-investment rights and direct access to founders. A fund of funds cares about your DPI timeline, portfolio construction, and reporting cadence.

Most managers waste months targeting the wrong LPs. They buy static lists, email hundreds of generic contacts, and wonder why their conversion rate is zero. You need to think about "portfolio construction" for your LP base. You do not just want money. You want the right mix of strategic backers who can provide follow-on capital, industry expertise, and introductions to subsequent LPs.

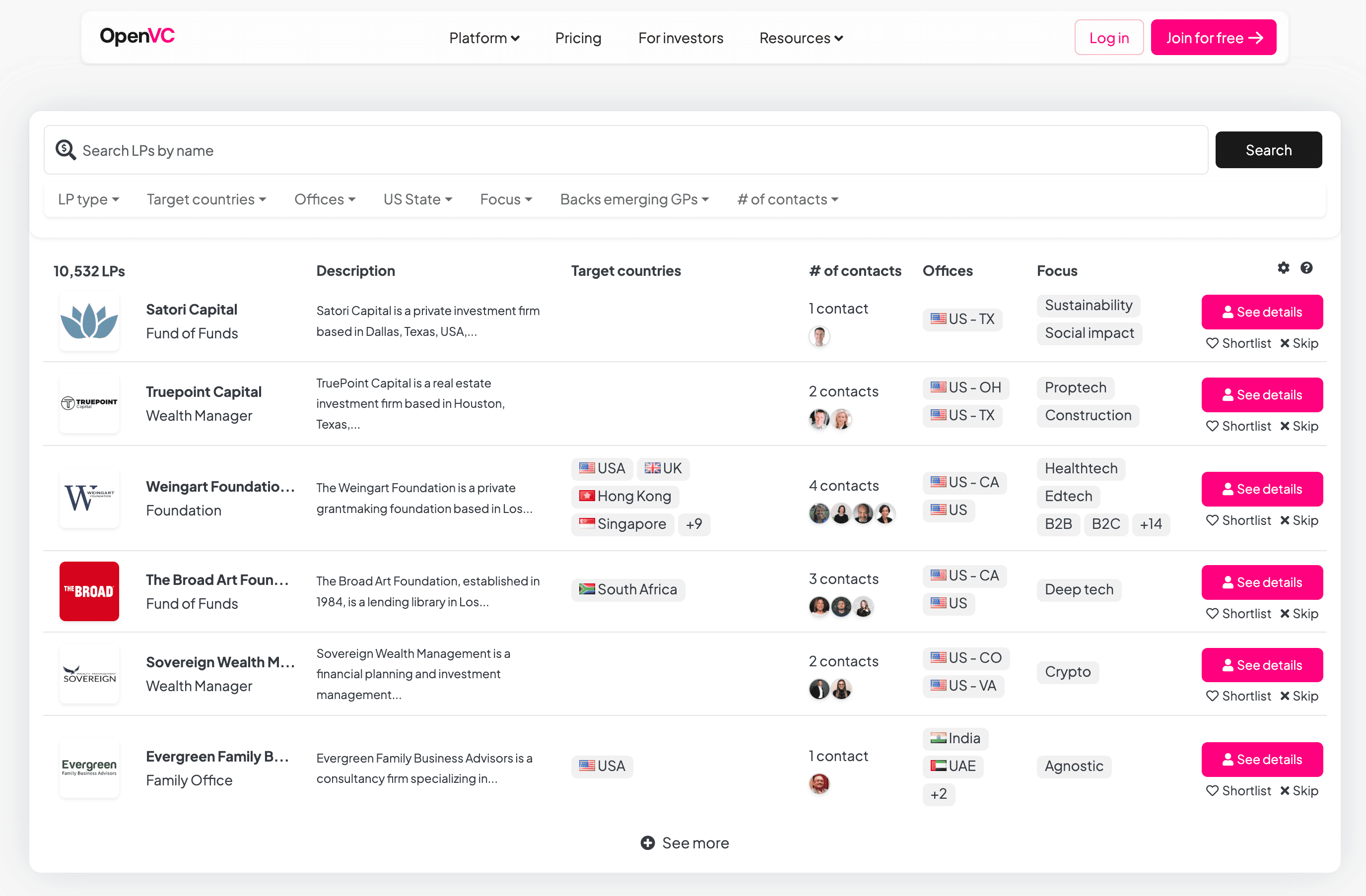

Building a targeted list shouldn't mean spending 100 hours manually scraping data into spreadsheets. This is where LP Navigator comes in. Using a verified database allows you to access LPs fast, filtering by geography, check size, and investment focus. It helps you identify which investors have backed similar funds so you can prioritize outreach effectively.

For deep dives on sourcing, review our resource on the Best LP Databases for Emerging Fund Managers.

Access the Right LPs, Without the 5-Figure Price Tag

Build a targeted LP list, get contact info or intro paths, and dive into outreach for just $300/month.

Running a Fundraising Process That Actually Moves

Fundraising is fundamentally a volume and consistency game. Once you have a highly targeted list, your focus must shift entirely to operations.

Adopt "pipeline thinking" for your raise. Every LP should fit into a clear stage:

- Identified

- Contacted

- Meeting scheduled

- Diligence

- Soft commit

- Closed

If an LP sits in the "diligence" phase for a year with no movement, they are a 'no'. Clear out the dead weight so you can focus on active conversations.

Long sales cycles are the biggest pain point in capital raising. You have to manage LP relationships over 6 to 12 months without being annoying. Provide actionable, concise updates. Do not email them every week asking for a decision. Instead, send them a quick note when you close a high-profile deal or when an existing portfolio company hits a major milestone.

A lightweight Fundraising CRM approach keeps these follow-ups structured. If you use a purpose-built tool rather than a chaotic spreadsheet, you prevent warm leads from going cold. You know exactly when you last spoke to an LP and what the next actionable step is.

Outreach, Intros, and Relationship Building

Warm introductions convert at a higher rate than cold outreach. That is a fact. But finding warm intros requires strategy. You have to map your network, identify shared connections, and provide forwardable emails to your mutual contacts. Make it incredibly easy for people to introduce you.

Cold outreach works, but you have to do it right. If you send a generic, five-paragraph email, it will be deleted. A strong cold email is brief, highlights your unique edge, references the LP's past investments, and asks for a short introductory call.

Relationship building starts long before the actual raise. Smart GPs practice "credibility stacking." This involves sending consistent, low-ask updates over time to build trust before ever asking for a check. If an LP has read your quarterly market update for a year and seen your predictions play out, taking a meeting for your Fund II becomes a logical next step rather than a cold favor.

Closing Capital and Maintaining Momentum

The hardest part of the fundraising process is getting to a " yes." An LP telling you they are "highly interested" means absolutely nothing. A "soft commit" is not legally binding and cannot be spent. Until the capital is called and the wire clears, you do not have the money.

You need practical ways to create urgency without applying cheap pressure. One of the best ways to force a decision is through a rolling close. By holding a first close, you create a real deadline. LPs know that if they wait, they might miss out on the initial deals or face different fee structures.

Warehousing deals is another powerful mechanism. If you secure an allocation in a highly competitive startup and offer it to early LPs, you shift the dynamic. You are no longer asking for capital; you are offering exclusive access.

Keep your momentum going across the months it takes to hold a final close by following a strict checklist:

- Schedule bi-weekly updates with all committed LPs.

- Share sanitized case studies or portfolio construction examples

- Leverage your committed LPs for introductions to their peers.

- Set clear, non-negotiable deadlines for subsequent closes.

The Emerging Manager Fundraising Checklist

Let’s recap everything we’ve covered and convert it into a clear, concise, actionable checklist for you.

- Define your LP profile: Know who you’re targeting. Match LP attributes like check size, investment focus, and risk tolerance to your fund’s strategy. A clear profile saves time and effort.

- Build a focused LP list: Skip the scattershot approach. Use verified tools like LP Navigator to identify LPs who align with your thesis or have backed similar funds.

- Map out your pipeline: Treat fundraising like sales. Organize LPs into stages (research, outreach, meeting, diligence, soft commit, and closed) to track progress and stay disciplined.

- Craft targeted outreach: Personalize your approach. Reference specific LP interests or past investments, and keep your message concise and compelling.

- Leverage your network: Warm intros > cold outreach. Strategically map your connections to get in front of the right people. A strong intro can open doors.

- Refine your pitch: LPs expect clarity and focus. Highlight your edge, fund thesis, and why you’re uniquely positioned to succeed. Tailor your story to their priorities.

- Follow up strategically: Keep LPs engaged with meaningful updates like new commitments or portfolio wins. Be persistent but respectful of their timelines.

- Adapt and iterate: Fundraising is dynamic. Use feedback to refine your approach, pivot if needed, and double down on what works.

- Focus on momentum: Create urgency with rolling closes, warehousing deals, or firm deadlines. Keep your pipeline moving, and don’t let warm leads go cold.

- Stay disciplined: Fundraising is a marathon, not a sprint. Stick to your process, track results, and stay consistent. Success comes to those who execute with precision.

By following this checklist and applying the strategies outlined in the guide, you’ll approach fundraising with confidence, clarity, and efficiency.

Stop Searching, Start Closing

Fundraising is a systematic process, not a black box. You cannot rely on a great track record alone to get your fund raised. You need a targeted strategy, a clean operational pipeline, and relentless consistency in your outreach and follow-ups.

Finding the right investors should not rely on gatekeepers or opaque country club networks. The data is out there, and the tools exist to help you move faster. Stop wasting time pitching generalist LPs who will never invest in your specific thesis.

Take control of your pipeline today. Use LP Navigator to discover verified LPs, identify warm introduction paths, and automate your workflow. Stop guessing, and start closing.

Access the Right LPs, Without the 5-Figure Price Tag

Build a targeted LP list, get contact info or intro paths, and dive into outreach for just $300/month.