"What if you could skip fundraising and go straight to M&A?

For early-stage startups, growth is the ultimate goal. While fundraising is often the default strategy, mergers and acquisitions (M&A) offer a compelling alternative—or complement—to traditional funding rounds.

M&A can help startups accelerate growth, acquire talent, expand market share, and even achieve a higher valuation than they could on their own. However, the process requires careful planning, research, and execution.

Here’s a quick guide to navigating M&A as an early-stage startup

Table of Contents

I. Is Early-Stage M&A Right for Your Startup?

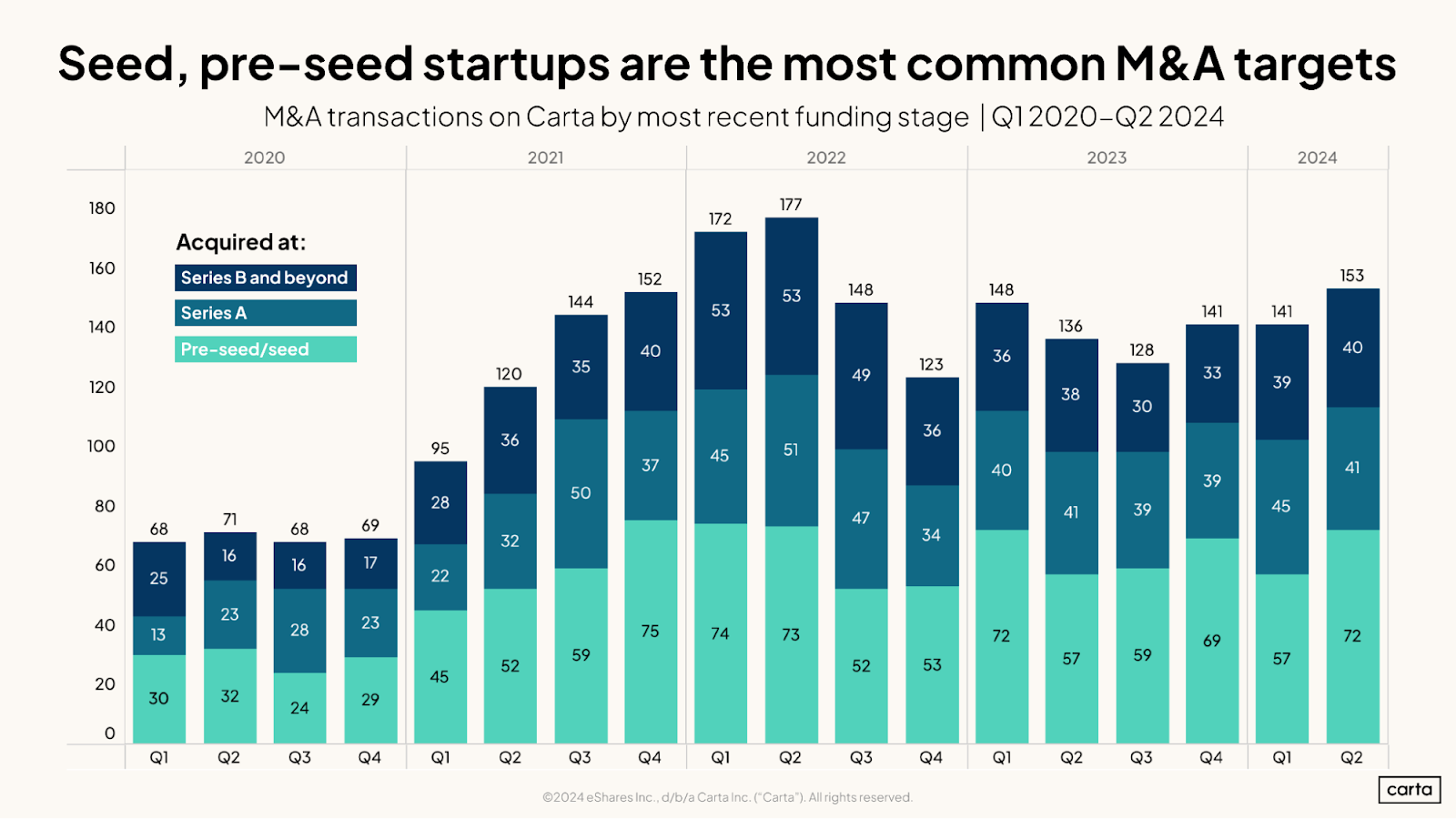

Generally, nearly half of early-stage startups exit or continue to grow via M&A. While large companies often make the headlines, many founders choose a strategic merger or acquihire to continue building their businesses—or to exit, if they prefer

But before diving into M&A, founders must assess whether this strategy aligns with their startup’s goals and current situation.

Here are some key questions to consider:

1. Can You Raise Funds in the Next Six Months? If so, at what cost?

Aside from simply struggling to fundraise in the current venture environment, there are multiple other situations where fundraising options are limited or will be limiting your business.

For example, a low expected valuation, especially in emerging markets, or other restrictive fundraising terms, such as a high liquidation preference. Or consider a capital-intensive company at an inflection point, where the actual struggle isn’t fundraising in general, but covering the liquidity gap until customers start paying, i.e. imbalanced cash flow due to the nature of the business.

All in all, the real question is: if you can fundraise, would it be enough to get to the next stage, and at what cost?

M&A might be a viable option, instead of or along with the fundraising round.

2. Do You Have Proprietary IP or Patents?

Intellectual property (IP) can significantly enhance your startup’s valuation and attractiveness to potential acquirers or merger partners. If you have proprietary technology or patents, M&A could be a way to monetize or scale your IP.

3. What Stage Is Your Product At?

The stage of your product development will influence the type of M&A deal you pursue. For example, a startup with an MVP might not be ready for M&A at all. A startup with a stronger product and proven market traction even if still early might easily merge with another startup of similar size. An operational product might be acquired by a notch larger company, whereas the teams will join forces and build a larger business together faster.

4. Would Acquiring Be More Efficient Than Building In-House?

Building new features or entering new markets in-house can be time-consuming and expensive. Acquiring a complementary product or a team can help you achieve your goals more efficiently. Same is true if you are building a b2c product and looking to expand into b2b in the future.

5. What’s Your Traction?

Realistically, a time to consider M&A is when you have reasonable market validation. It might be just $100k/year, but you can already clearly see that at least one of the sales channel works and scales, and you can grow within a specific market segment. Normally, it happens around the seed stage.

With deeptech startups it’s a bit more complicated. You want to be at least at TRL5/6, with revenues or LOIs or pilots or similar.

6. Do You Have Investors & The Board?

While you don’t have to call the board meeting to simply start looking for potential M&A alliances, you need to make sure that your entire cap table is on the same page on this strategy. The worst thing you can do is spend months pursuing a deal only to be blocked by one of your board members.

Unfortunately, this happens from time to time, and not always for a good reason. We have seen great deals blocked simply because an investor wanted to impose their own vision to the point where the founders eventually had to buy that investor out

It’s a bit easier for bootstrapped startups or startups where they own most of the company. Still, you need to align the strategy with all stakeholders.

7. What’s Your Areas of Most Synergy? What Won’t You Do?

If you have access to a specific market (geo, vertical) and are exploring novel business models or looking to build a product faster, M&A might be a great response to any of these goals. However, you need to clearly outline the areas you want to address through this transaction and how it aligns with your long-term vision.

Similarly, you will have a list of no-goes, which can be anything from rebranding to becoming someone’s department. All these limitations will simply help to outline the best potential partners early.

II. Early-Stage Deal Types: Merger, Acquisition, or Acqui-Hire?

Early-stage startups typically pursue one of three types of M&A deals:

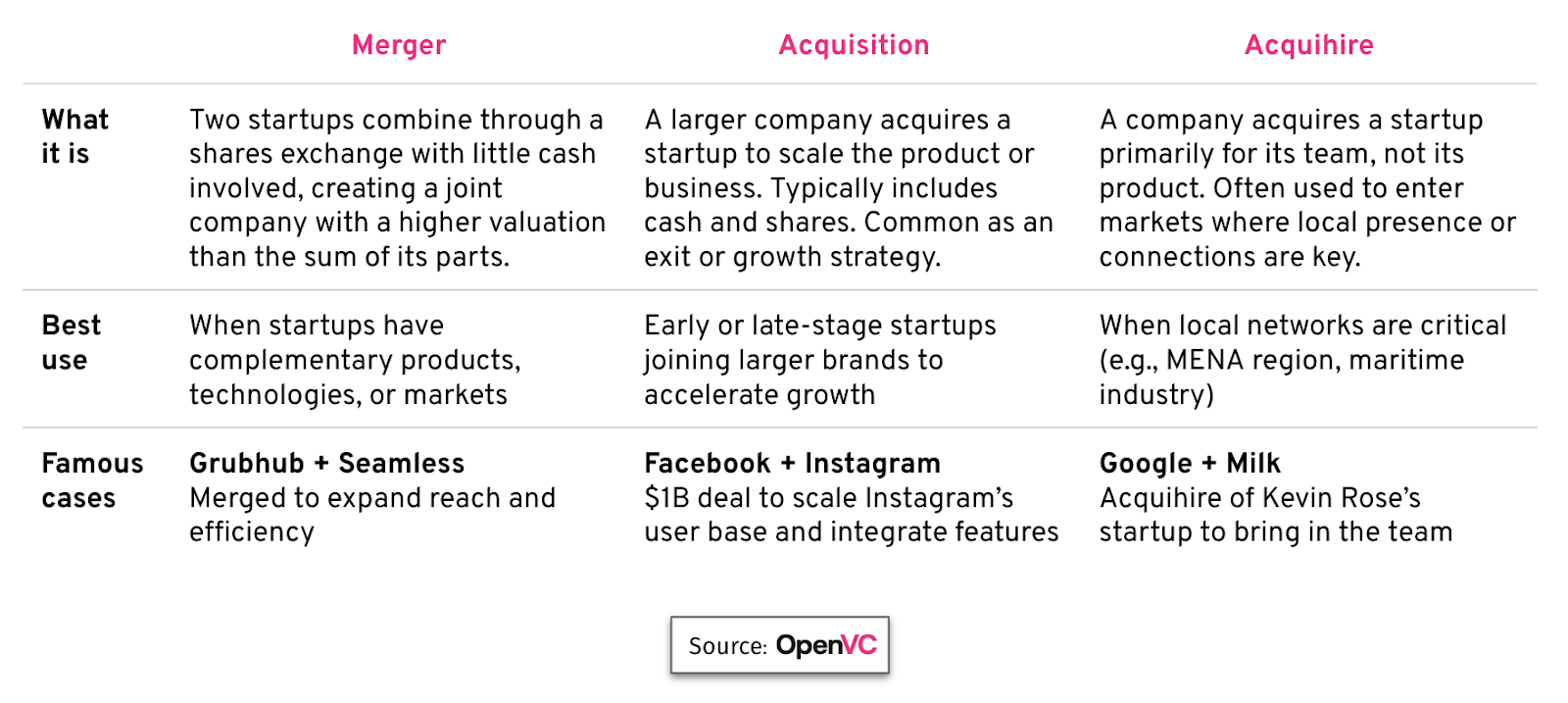

1. Merger

In a merger, two startups combine through a shares exchange, with no cash or almost no cash involved. The goal is to create a joint company with a higher valuation than the sum of its parts. Mergers are ideal for startups with complementary products, technologies, or market presence.

2. Acquisition

In a strategic acquisition, a larger company acquires a smaller startup to scale its product or business faster. The deal usually involves a combination of cash & shares. While we usually see this deal type as an exit strategy for late-stage startups, early-stage companies can exploit this as a growth strategy (at series A, for example). Continuously building your product while being a part of a larger brand with more resources at hand.

3. Acquihire

An acquihire involves buying a startup primarily for its talent. The deal typically includes higher cash components. It’s especially valid when you need to expand in the market where local network / very specific connections are important, and sales won’t happen if you simply open a legal entity. It might be presence in MENA or expansion in maritime business.

III. Going alone or hiring an M&A advisor?

There are certain situations where you can handle the entire process yourself. Namely,

- You already know the founders of another company well or your market is too specific, so you already understand who to talk to

- You have decent experience in M&A / JV / acquihires / franchises and understand how those can be structured & negotiated

- You have enough spare time to run the entire process

- The transaction size is relatively small (typically, less than $3M in value) so paying any extra fees won’t make much economic sense

On the other hand, a M&A specialist can help you

- Expertise in deals of this type, on valuations, DD, termsheets, legal paperwork

- Expand a network & find suitable partners esp. cross-border

- Take off the workload on the entire deal process, from search to closing so you can concentrate on building your own business first

- See red flags and/or misalignment and/or potentially bad terms much earlier so you don’t waste the time on talking to the wrong companies

- A negotiations buffer, including emotionally.

On costs:

- Going alone is first of all, the cost of the time you are going to spend, which is pretty similar to fundraising - a separate full time job for at least one co-founder. That, and legal expenses.

- M&A advisors usually have at least two different models: cash only (retainer & success fee; but depending on the stage, even retainer might be price-prohibitive), - or cash & equity (some costs covered / prepayment, and a stake in a company post deal), which is more aligned with early-stage startups.

When it comes to actual pricing, advisors will ask anything between thousands a month in retainer + 2-3% finder fee to a 10% finder's fee. The range is huge and transparency is low.

IV. Roadmap: The M&A Process Step-by-Step

The M&A process for early-stage startups typically follows a structured roadmap. Here’s a detailed breakdown of each step:

1. Self-Assessment

Before you start looking for potential partners, conduct an honest self-assessment of your startup’s strengths, weaknesses, and strategic gaps. This will help you identify what you’re looking for in a deal and what you’re willing to compromise on.

- Minimal Viable Team at the next stage : Identify any gaps that could be filled through M&A.

- IT and Product Roadmap : Determine which parts of your development and product roadmap you should achieve in-house, and which might be easily obtained via M&A, including costs comparison.

- Go-to-Market Strategy : Estimate the costs and time required for entering your next market segments.

- Legal and Regulatory Matters : What’s your requirements in new markets, and what’s the easiest way to obtain those.

- Governance : Decide which roles you must keep and which you’re willing to delegate or negotiate over.

- Finance : Prepare a clear budget for the next 12-24 months, including financial projections.

- Investors : Any limitations known + any board voting / similar limitations

- Deal type that’s preferable to you, your investors and your board – what realistically you want to do, and what you can defend

2. Search for Potential Targets

Once you have a clear idea of who you're looking for, begin searching for potential M&A targets. Focus on companies that complement your strengths and fill your strategic gaps. At this stage, you'll likely have a long list of potential companies. You’ll narrow it down during the research stage and further as you conduct preliminary due diligence.

- Strategic Gaps : Look for companies that can help you address gaps in your product, IT, regulatory, GTM strategies.

- Complementary Areas : Identify companies with complementary products, technologies, or market presence.

- Long Negotiations. Prolonged negotiations can kill deals. Set clear timelines and milestones to keep the process on track.

3. Pre-Due Diligence

Of all the companies you have researched, you should be able to shortlist some as main potential partners. Preliminary due diligence helps to shorten the list further before you reach out to anyone.

- Risk mitigation: known aggressive competitors, companies about to shut down, latest known valuation was years ago or was too high, big disparity between revenue numbers of the same stage companies and so on. All of the above would be a deal blocker for a variety of reasons.

- Team Assessment : Research the target company’s founders, team and investors. Researching their investors’ portfolios might be helpful as well.

- Financial Estimates : Try to estimate the target’s financials based on available data. At the very least, you should be able to assess the company's size overall (users, revenues, latest investments). Would they agree to even talk to you?

- Product and IT Compatibility : Evaluate the target’s product and technology to identify potential synergies and overlaps.

- Long Negotiations. Prolonged negotiations can kill deals. Set clear timelines and milestones to keep the process on track.

- Market Presence : Analyze the target’s market presence and business model to identify potential synergies.

Once your short list is formed and checked, start the reach out aiming for introductory calls only : informal calls between founders’ help assess whether there’s a cultural and strategic fit before disclosing any sensitive information, and avoid wasting everyone’s time.

All in all, it’s beneficial to have an M&A partner at this stage (or preferably earlier), since M&A negotiations are private, and you’ll likely want to avoid any news leaking prematurely. An M&A partner will reach out to companies on your behalf without disclosing your name until they deem it reasonable and under NDAs.

4. Negotiations

This stage can take anywhere from a few weeks to months, depending on the complexity of the deal and, naturally, the human factor. Go from one call to another, don’t rush it. Getting to know each other as well as being fully aligned is crucial.

- Team Strategic Gaps

- Option Pool : Set aside an option pool for future hires.

- Governance : Everything that requires approval – from team roles to joint investors & board.

- Strategic gaps: What can you cover and what the other company can cover on technology, product, sales, regulatory and so on?

- Complementary areas: What will you continue developing and what will they? How do sales synergize?

- Go-to-Market Strategy : Develop a joint go-to-market strategy that leverages the strengths of both teams.

- Legal Setup : Explore options for structuring the joint company, considering any legal limitations.

- Regulatory: How easily would you be able to use the other company's regulatory setup and vice versa?

- Financial Model : Create a joint financial model and budget for the first six months post-deal.

Important note: don’t shy away from disagreements, be open to differences of opinions, and give it time. If it’s not resolved, you will see it fast enough (2 nd -4 th calls) and simply will not proceed in negotiations.

Taking each new call as one step at a time where you both have freedom to say no, helps you to move faster with greatly suitable teams, and drop out of negotiations when any clear misalignment arises.

5. Terms and Valuation

The terms of the deal are critical to its success. Pay close attention to the details, as human ego and superficial terms can derail even the most promising deals.

- Valuations : Agree on the valuations of both companies and the conversion ratio for shares. Generally, M&A valuations aren’t your latest venture rounds, those are business valuations, based on revenues, IP, licenses and so on. However, the idea is that your next venture valuation as a joint company will be larger than 1+1 and will give you leverage – and a choice.

- Conversion structure : shares, or shares and cash.

- Investor Terms : Negotiate terms for existing investors, including deadlines for approvals and signatures. Outline any deadlines for what needs to be approved & signed, especially via the board.

- Option Pool : Set aside an option pool for future hires.

- Specific Terms : Address any specific terms for individual founders or investors, such as buyout options for early investors or advisors, change of roles of the joint team – the list is long.

- Term sheet and the outline of the full paperwork

Normally, at this stage you would draft a presentation for all your stakeholders on how the potential joint company would look like (strategy, finance, valuations, next steps). That helps to communicate with everyone enormously.

Human ego kills many deals; superficial terms and extremely long negotiations kill as many.

6. Due Diligence

Before proceeding with the full paperwork, both parties must complete a full due diligence process. This step ensures that all aspects of the deal are transparent and that there are no hidden surprises. Normally, all your stakeholders will be helping you at this stage. The full dd list should be familiar to you already, with certain differences between industries and geographies.

Since we are discussing M&A for early-stage startups, there is no good reason to spend a month or two on a full-blown dd unless you have at least an initial confirmation that the deal is on, and it makes sense at all.

Research will help you filter all the unsuitable companies and introductory calls will cut the choice down to just a handful of companies. Finally, preliminary dd exists for a reason – spend a reasonable amount of time to make sure you won’t be talking to fraudsters.

Normally you would end up with 2-5 companies even before reaching out.

7. Post-Deal Integration

Once the deal is signed, the real work begins. Successful post-deal integration is critical to realizing the full value of the M&A transaction. While likely you already have a lot of ideas and joint presentations at this stage, you would now be moving as a single unit, so properly working out all the details is important.

- Legal Actions : Complete any necessary legal actions, such as reincorporation or tax considerations.

- Joint Org Chart : Develop a joint organizational chart and ensure that both teams work well together.

- Governance : Establish a joint investor board or governance body and ensure that all members are aligned.

- Go-to-Market Strategy : Prioritize go-to-market initiatives that leverage the strengths of both teams.

- Governance : Establish a joint investor board or governance body and ensure that all members are aligned.

- Long Negotiations. Prolonged negotiations can kill deals. Set clear timelines and milestones to keep the process on track.

Risks and Mitigation Strategies

M&A is not without risks. Here are some common pitfalls and how to avoid them:

- Competitors Shopping for Information. Be cautious when approached by competitors or their investors. Conduct thorough research to ensure that the other party is genuinely interested in a deal, not just gathering information.

- Human Factor. Many deals fall through due to mismatched cultures or egos. Focus on building trust and rapport during introductory calls and further negotiations.

- Superficial Terms. Pay attention to the details of the deal terms. Superficial or poorly defined terms can lead to disputes down the line.

- Long Negotiations. Prolonged negotiations can kill deals. Set clear timelines and milestones to keep the process on track.

M&A as a Growth Strategy

M&A is not just an exit strategy for big players, it’s a way to accelerate product growth, access new markets, and build a stronger, more competitive business for earlier startups.

With the right approach, early-stage startups can leverage M&A to achieve their long-term goals and create lasting value, while preserving cash, avoiding unnecessary dilution, launching in their respective markets faster and cheaper, while having a stronger leverage in their next fundraising rounds.

About the author

Trader and asset manager turned founder, operator and investor, working at the intersection of science, technology, culture and education for the last 15 years, with a background in institutional asset allocation. Worked with over a 100 of early stage startups from edtech, fintech, HRtech, robotics, hardware, proptech, creative industries, clouds, music tech, A& and Big Data etc across developed and emerging markets, as well as with VCs, venture studios, accelerators and corporates. Currently Olga Duka is a GP at Improve Ventures, focused on cross-border M&A as a growth strategy for early stage startups, supported by OpenVC.